7 October 2025

What is VAT and how does it work in the UK?

VAT is a consumption tax levied on most goods and services sold within the UK. It is not a tax on your business’s profits, but a tax on the value added at each stage of the supply chain. You can think of it as a transaction tax that is ultimately paid by the end consumer.

Your role as a business is to collect it from your customers and pay it over to HM Revenue & Customs (HMRC), minus any VAT you have paid on your own business purchases.

The mechanism is straightforward. If your business is VAT-registered, you must charge VAT on the taxable goods or services you sell. This is your ‘output tax’. Conversely, you can reclaim the VAT you pay on goods and services you buy for your business (from other VAT-registered suppliers). This is your ‘input tax’.

When you complete your VAT return in the UK, you calculate the difference between the output tax you’ve collected and the input tax you’ve paid. If you’ve collected more, you pay the difference to HMRC. If you’ve paid more, you can claim a refund. This system ensures the tax is borne by the final consumer, not the businesses in the chain.

UK VAT registration: Requirements and process

Not every business must register for VAT immediately. The requirement is triggered when your business’s taxable turnover exceeds the VAT registration threshold. This threshold is currently £90,000 (as of the 2024/25 tax year) and is reviewed annually.

It’s crucial to monitor your rolling 12-month turnover, not just your annual turnover from April to April. The moment you realise your turnover has exceeded the threshold, you have 30 days to register.

However, voluntary registration is also an option, even if your turnover is below £90,000. There are strategic reasons to do this. It makes your business appear larger and more established, and it allows you to reclaim VAT on your start-up costs and other business expenses. This can significantly improve your cash flow, especially in the early days.

The process for VAT registration in the UK is conducted online through the HMRC Government Gateway. You will need your:

- National Insurance number

- Details of your business (turnover, bank details, nature of business)

- Unique Taxpayer Reference (UTR) if you are already registered for self-assessment

Once your application is processed, HMRC will send you a VAT registration certificate with your unique VAT number, which you must then display on all your invoices.

You can expand to the UK by seeking our professional advice. You’ll have direct access to local experts, who can help you understand the VAT registration process.

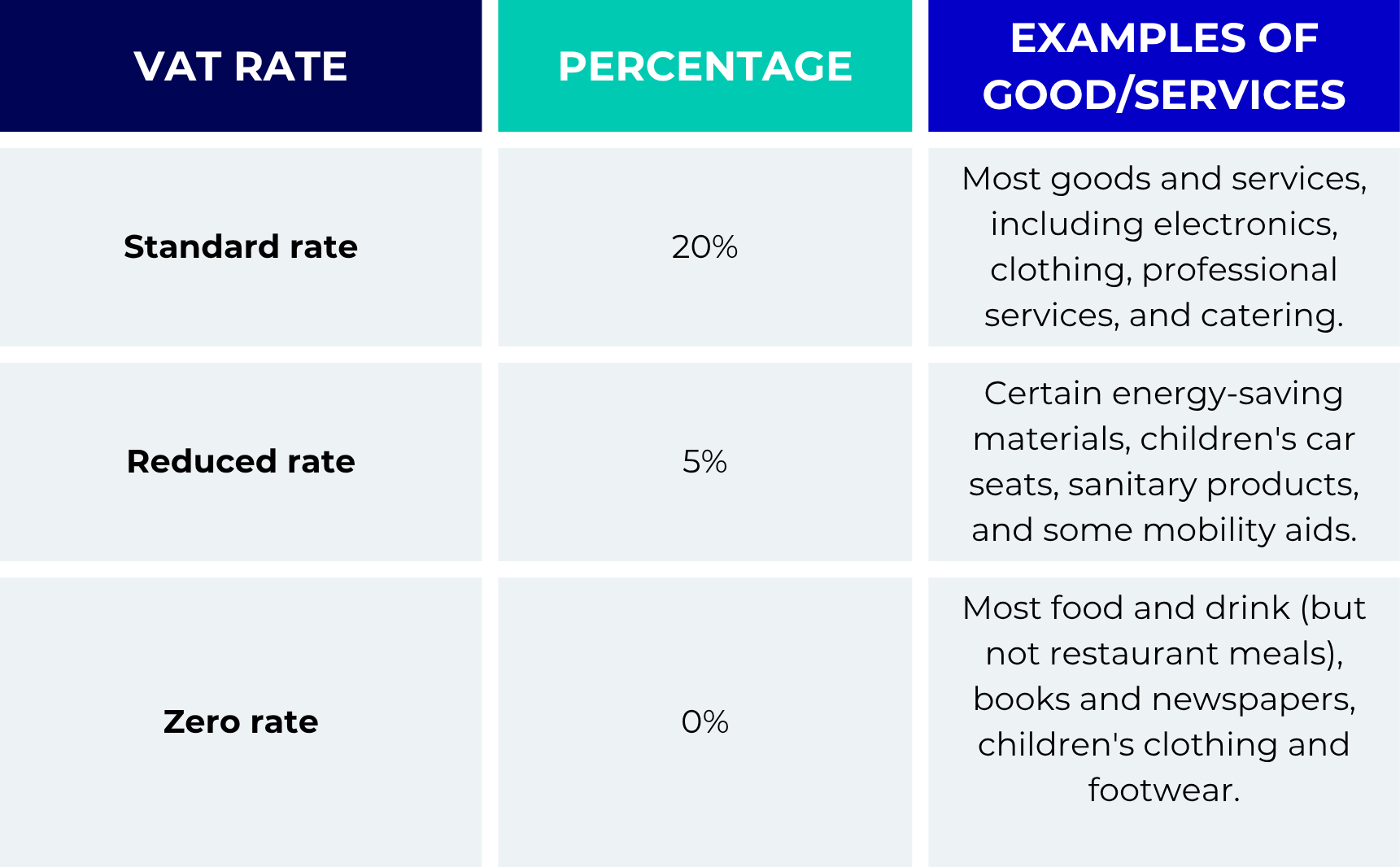

Understanding VAT rates in the UK

There are three main rates of VAT in the UK. Knowing which rate to apply is a core part of your VAT compliance obligations. Charging the incorrect rate is a common error that can lead to complications with HMRC.

Note: It is vital to note that ‘zero-rated’ and ‘exempt’ are not the same. Zero-rated supplies are still taxable, meaning you must record them on your VAT return and can reclaim the related input VAT.

If you’re working independently and need help understanding tax rates, you can opt for our umbrella company model. It’s a solution that lets you contract legally in the UK without setting up your own entity.

VAT returns and deadlines

Filing a VAT return is a quarterly task for most businesses. This process summarises your sales and purchases, and calculates the VAT you owe to HMRC or are owed as a refund. Your VAT return must be submitted online. Also, any payment must be made electronically, typically by direct debit.

Your specific deadlines are determined by your VAT ‘stagger’, which HMRC assigns upon registration. You are given a quarter-end date and a deadline for submission and payment. These are always one calendar month and seven days after the end of your VAT period.

For example, if your VAT quarter ends on the 30th of June, your return and payment are due by the 7th of August. This is a strict deadline. Late submission triggers a penalty point system, and once a threshold is reached a £200 penalty is issued. Furthermore, late payments result in interest charges and potential surcharges, making it imperative to stay organised.

Special VAT schemes in the UK

To simplify the process, especially for smaller businesses, HMRC offers several special schemes:

- Flat rate scheme: This scheme can simplify your bookkeeping. Instead of recording the VAT on every purchase and sale, you pay a fixed percentage of your total VAT-inclusive turnover. The percentage depends on your industry. The benefit is simplicity and potentially keeping the difference between what you charge your customers and what you pay to HMRC. However, you generally cannot reclaim VAT on purchases, except for certain capital assets over £2,000.

- Annual accounting scheme: This scheme is designed to improve cash flow. Instead of filing four returns a year, you file one annual return. Also, you make monthly or quarterly instalments based on an estimated VAT bill. The balance payment is due when you submit your annual return. This is ideal for businesses with stable turnover and are looking for tax advantages.

- Cash accounting scheme: Under this scheme, you account for VAT based on when you actually receive payment from your customers and pay your suppliers, rather than on the invoice date. This can be a significant help for cash flow if you have slow-paying clients. That’s because you don’t have to pay VAT to HMRC until you have the cash in your account.

VAT considerations for expats and small Businesses

For expats, understanding VAT rules in the UK adds an extra layer of consideration. If you are based in the UK and supplying services to clients here, the standard UK rules apply. However, if your clients are based overseas, the place of supply rules often mean the transaction is outside the scope of UK VAT.

For all small businesses, maintaining meticulous records is the cornerstone of VAT compliance. Keep all sales and purchase invoices organised. Furthermore, understand the correct VAT rate for your sector, and diarise your deadlines. Using accounting software can automate much of this process and drastically reduce the risk of error.

Summary

Mastering VAT in the UK is a non-negotiable aspect of running a compliant and successful business as an expat. It demands attention to detail to meet those all-important filing deadlines. While the system is designed to be logical, its administrative weight can be heavy for a solo entrepreneur or a small startup focused on growth.

This is where professional support becomes invaluable. For professionals and businesses alike, an Employer of Record in the UK service can be a powerful solution. An EOR handles all complex legal, tax, and compliance issues on your behalf.

It includes VAT, payroll, and other tax obligations. This allows you to focus entirely on your core work, secure in the knowledge that your VAT compliance obligations are being managed expertly and on time. It frees you from the administrative burden and lets you concentrate on what you do best. Contact us to learn how we can support you.

Frequently asked questions

As an expat freelancer, when must I register for VAT?

You must register for VAT if your total taxable turnover from services supplied within the UK exceeds the £90,000 threshold in any rolling 12-month period. You can also register voluntarily to reclaim VAT on your business expenses. That’s often beneficial even if you are below the threshold.

How do I charge VAT to clients in other EU countries?

For B2B services, the place of supply is your client’s country. Hence, you do not charge UK VAT but must instead include your UK VAT number on the invoice. Also, you may need to complete an EC Sales List. Your client accounts for the VAT in their own country.

What are the penalties for submitting a late VAT return?

HMRC operates a penalty points system. Each late return earns a point. Once you reach a threshold (4 points for quarterly returns), you receive a £200 penalty. Further penalties of £200 are issued for every subsequent late submission while at the threshold. Note that late payments also incur interest.

Can I reclaim VAT on things like my laptop or office furniture?

Yes, if your business is VAT-registered, you can typically reclaim the VAT paid on goods and services used exclusively for your business. This includes equipment like laptops, office furniture, and software subscriptions. However, you must keep the original VAT invoices as proof of purchase.

What is the difference between the Flat Rate and Standard VAT scheme?

Under the Standard Scheme, you pay HMRC the difference between the VAT you charge customers and the VAT you pay on purchases. The Flat Rate Scheme simplifies this. You pay a fixed percentage of your total turnover and generally cannot reclaim VAT on purchases.