10 June 2025

How to set up a business in the UK: What international companies need to know

The United Kingdom remains a highly attractive destination for international companies. Whether it’s access to a skilled workforce, a business-friendly regulatory environment, or proximity to key global markets, the UK offers compelling reasons for expansion.

However, setting up a business in a new country requires careful planning and consideration. You need to understand the legal structures available, the regulatory requirements, and the tax obligations that come with operating in the UK. If you’re looking for a faster and more flexible way to start operations or hire employees in the UK, working with a British Employer of Record can offer a compliant solution without the need to set up a legal entity.

In this guide, I’ll walk you through the key steps to set up a business in the UK, and introduce an alternative option for companies that want to start operating or hiring without the complexity of forming a legal entity.

Choosing a legal entity structure

The first major decision you’ll face when expanding into the UK is choosing the right business structure. Each option comes with its own legal, financial, and operational implications.

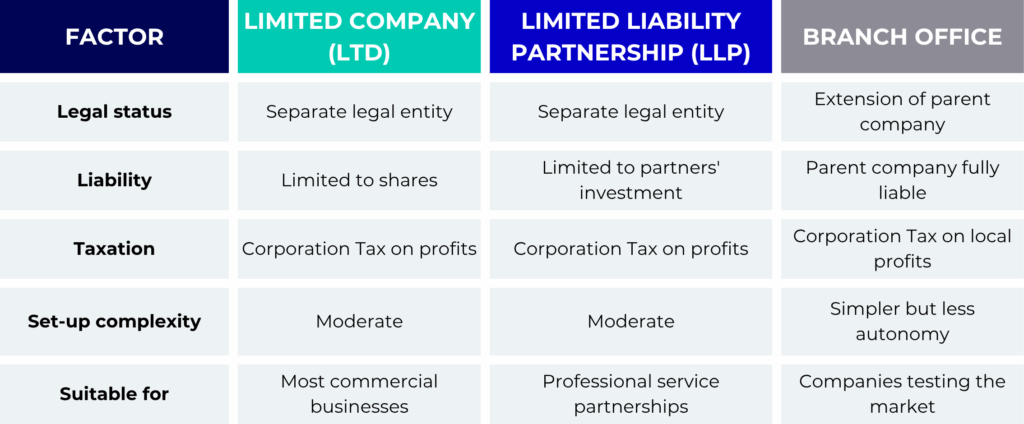

Here’s a breakdown of the most common entity types for foreign companies:

Limited Company (Ltd)

This is the most popular option for private businesses entering the UK. A Limited Company is a separate legal entity from its owners, which limits the liability of shareholders to the value of their shares. It’s suitable for most commercial activities and offers credibility with customers, suppliers, and partners.

Limited Liability Partnership (LLP)

Typically used by professional service firms, an LLP provides flexibility in internal governance and protects the personal assets of its partners. It is popular among law firms, accounting firms, and consulting firms.

Branch office

A branch is not a separate legal entity but rather an extension of a foreign parent company. While it’s quicker to set up than a Limited Company, it does not offer the same separation of liabilities, and the parent company remains fully responsible for the branch’s activities.

Comparing the options:

Choosing the proper structure depends on your business goals, the permanence of your expansion, and your risk tolerance.

Registering your business with Companies House

Once you’ve chosen a structure, you must register your entity with Companies House, the UK’s registrar of companies.

For a Limited Company or LLP, the process involves:

- Choosing a company name and checking its availability.

- Preparing a Memorandum and Articles of Association (Ltd) or LLP Agreement (LLP).

- Providing details of shareholders, directors (for Ltds), and partners (for LLPs).

- Specifying a registered office address within the UK.

You can register online or through an agent. Registration usually takes 24 to 48 hours if submitted electronically, with a registration fee of £12 (subject to updates).

Once registered, your company must meet ongoing compliance requirements, including:

- Filing an annual confirmation statement.

- Submitting annual accounts to Companies House.

Keeping statutory registers of directors and shareholders.

Registering for tax with HMRC

After you’re registered with Companies House, your next step is tax registration with HM Revenue & Customs (HMRC). Depending on your business activities, you may need to register for several taxes:

- Corporation Tax: All companies must register for Corporation Tax within three months of starting business activities. Corporation Tax is currently charged at 25% (subject to changes), applied to your taxable profits.

- PAYE (Pay As You Earn): If you plan to hire employees, you must register as an employer with HMRC and operate a PAYE scheme to withhold income tax and National Insurance Contributions from salaries.

- VAT (Value Added Tax): If your taxable turnover exceeds the VAT threshold (currently £90,000), you must register for VAT. You can also register voluntarily if your turnover is below the threshold, which can be beneficial for reclaiming VAT on business expenses.

Each tax type comes with its own registration deadlines and reporting requirements. Corporation Tax filings, VAT returns, and payroll submissions must all be done in a timely manner to avoid penalties.

Other setup considerations for international businesses

Beyond registering your company and setting up your tax obligations, there are several important practical steps to take before you can begin operating smoothly in the UK.

Opening a UK business bank account is essential, but most banks will require proof of business registration, a UK address, and identification documents for company directors or LLP partners. This process can take time, so it’s advisable to prepare all necessary documents early.

Another key requirement is having a registered office address within the UK. This can be a physical office, a serviced office provider, or a registered address service. The address will be publicly available on the Companies House register and must be maintained throughout your business’s existence.

Although not legally mandatory, appointing a UK-based director or local representative can simplify many administrative processes. Having someone on the ground often makes dealings with local authorities and banks smoother and can enhance the company’s credibility with customers and partners.

You should also be aware of sector-specific licences or regulatory requirements depending on your planned activities. Specific sectors, such as financial services, food businesses, or import/export operations, require additional permissions or adherence to specific regulatory frameworks. It’s crucial to check industry-specific requirements early to avoid delays in launching your business.

How British Employer of Record simplifies UK business setup

While setting up a legal entity in the UK is a well-defined process, it can still be time-consuming and administratively heavy, particularly if you need to hire employees quickly or test the market without committing to a full-scale operation.

That’s where a British Employer of Record comes in.

An EOR allows your company to:

- Hire UK employees legally without setting up a company or branch.

- Manage payroll, tax deductions, and employment benefits in full compliance with UK law.

- Draft compliant employment contracts and manage HR responsibilities on your behalf.

For example, when a Canadian fintech company decided to expand into the UK, they faced the usual challenges, lengthy company formation, regulatory approvals, and the need to hire a sales team quickly. Instead of waiting months to set up a subsidiary, they partnered with a British Employer of Record.

The EOR enabled them to hire and onboard local staff within weeks, ensuring compliance with UK employment laws, handling payroll and taxes, and providing employee benefits. This allowed the company to start building its UK market presence immediately, without the financial and administrative burden of creating a legal entity. Within a year, after validating the market, they moved forward confidently with setting up a full subsidiary, but only once their initial risk was minimised.

The EOR becomes the legal employer, while you control the employee’s day-to-day work. This setup is ideal for:

- Companies want to test the UK market before making a full commitment.

- Organisations need to onboard employees quickly without administrative delays.

- Businesses are aiming to reduce risk and simplify compliance.

By working with British Employer of Record, you can bypass the incorporation process entirely — saving time, money, and resources, while still having a compliant, local workforce.

Set up a business in UK

Expanding into the UK can be a strategic move for international businesses, but it requires a clear understanding of the legal, tax, and operational steps involved in setting up. Whether you form a Limited Company, an LLP, or a Branch Office, the process involves careful compliance with Companies House and HMRC requirements.

However, if your priority is speed, flexibility, and reduced overhead, partnering with a British Employer of Record may be the smartest path to take.

Need help deciding whether to set up a UK entity or use an Employer of Record? Contact our team to explore the best solution for your business expansion.